Relative Calm for the Stock Market

The stock market has been more calm in 2023 than last year, with the range between the market’s high and low about half what we saw for each quarter of 2022. A “range-bound” market suggests there is disagreement about which direction the market should be heading. Which narrative will prevail?

- The Bull Case: As inflation continues its downward trend, the Fed will be able to pause or even begin lowering interest rates which will help stimulate the economy.

- The Bear Case: If inflation remains high, the Fed will need to raise interest rates further and risk pushing the economy into a recession.

Tech’s Rebound

The technology sector has been the market’s best performer through the first quarter of 2023, growing by 21.4%. This recovers half of tech’s losses from 2022. Since the technology sector accounts for about one quarter of the S&P 500, its strong performance helped the S&P 500 grow 7% for Q1.

Large, Sudden Drop in Bond Yields

In contrast to the recent calm of the stock market, the bond market experienced some large, sudden changes. Following the Silicon Valley Bank failure and related worries about potential contagion throughout the financial sector, the yield of a 2-year treasury bond dropped from 5.05% to 3.93% in a single week!1 Since bond yields are inversely related to bond values, this was good news for those who own bonds (although it means slightly lower rates to reinvest in for the future).

Where are Interest Rates Headed?

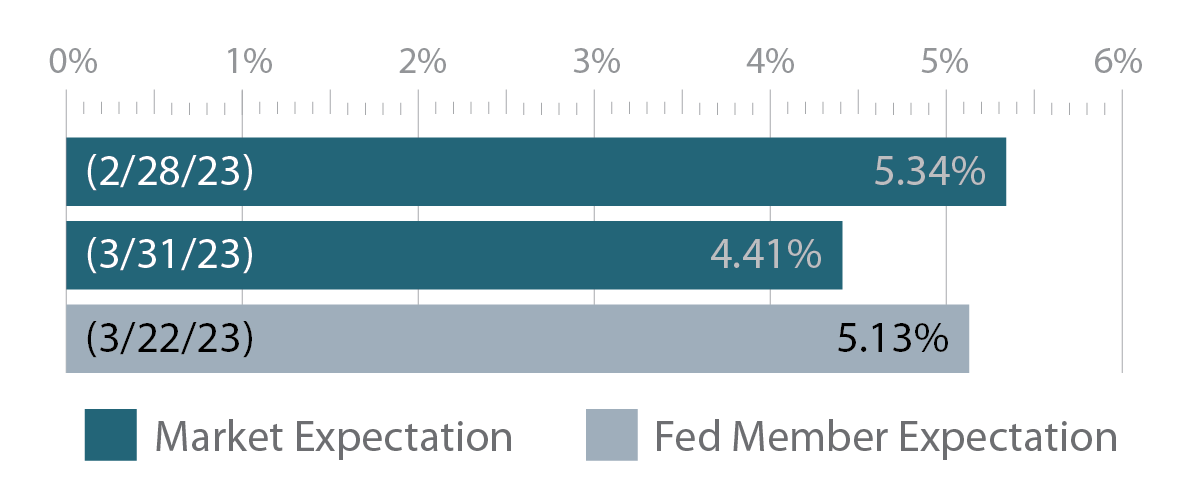

The market is now anticipating that the Fed will actually reduce rates by 0.42% by the end of the year, whereas just a month ago the market was expecting an increase of 0.51%.2 However, the members of the Fed, when polled, still believe that rates will end the year 0.30% higher.3 Either the Fed or the market will have to flinch in the coming months, so stay tuned.

Calm Before the Storm?

It appears inflation has peaked and is trending downward, and the labor market remains strong.5 This is good news and the market has celebrated seeing some light at the end of the tunnel.

However, inflation is still well above the Fed’s target and it remains to be seen whether the Fed will need to take further action. The relative strength of the economy gives us hope that a potential recession, if one occurs, could be short-lived and not very deep.

It’s prudent to proceed with caution. We will keep following the latest economic data and remain steadfast in our management of market risks, understanding that investors are rewarded in the long-run for staying in the market.

Sources & Disclosures

Data about the S&P 500 Index and Morningstar US Technology Index used from Kwanti.com

[2] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

[3] https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20230322.pdf

[4] https://www.newyorkfed.org/markets/reference-rates/effr

[5] https://www.bls.gov/charts/consumer-price-index/consumer-price-index-by-category-line-chart.htmand https://www.bls.gov/news.release/empsit.nr0.htm

Integral Investment Advisors, Inc. dba Integral Wealth Management is a Registered Investment Adviser. This material is for informational and illustrative purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Advisory services are only offered to clients or prospective clients where Integral Wealth Management and its representatives are properly licensed or exempt from licensure. The views and opinions expressed in this material reflects the personal opinions, viewpoints, and analyses of Integral Wealth Management employees and/or the individual providing such comments, and should not be regarded as a description of advisory services provided by our firm or performance returns of any our firm’s clients. The views and opinions expressed in this material is subject to change at any time without notice. Nothing in this material constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Our firm manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the material.

This material is developed from sources believed to be providing accurate information; no warranty, expressed or implied is made regarding accuracy, completeness, legality, reliability, or usefulness of any information. Integral Wealth Management may also provide links for your convenience throughout the material to websites produced by other providers of industry-related material. Accessing websites through links directs you away from our content. Our firm is not responsible for errors or omissions in the material on third party websites, and does not necessarily approve of or endorse the information provided. Users who gain access to third party websites may be subject to copyright and other restrictions on use imposed by those providers and assume responsibility and risk from use of those websites.

It is important to note that all investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance is not a guarantee of future results. Our firm urges you to please seek advice from your licensed financial professional prior to making any investment decision.