It’s hard to believe we’re already half-way through 2025! The markets came roaring back in the second quarter despite facing lots of adversity. Headline risks abound but the market has continued to be resilient and post new highs. Here’s a quick summary of how the markets have fared in the first half of 2025 and what to look for in the months ahead.

A Resilient Stock Market

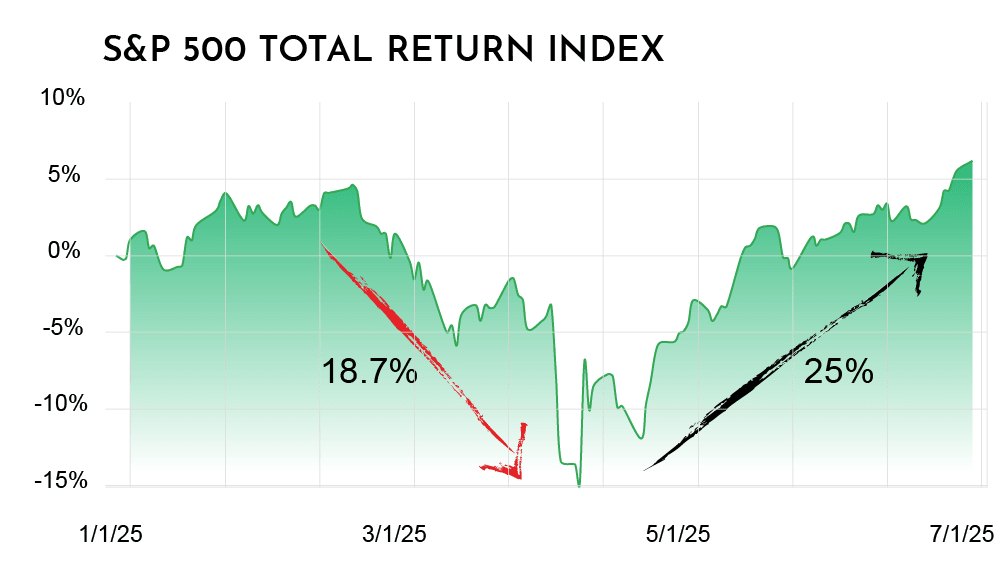

The stock market returned 10.94% in the second quarter, bringing the return for the first half of 2025 to 6.20%.1 What’s notable, however, is the path it took to get there. To begin the second quarter, the market accelerated its decline following the announcement of larger-than-expected tariffs, plunging to a level 18.7% below its mid-February high.1 The market rebounded sharply when a lengthy pause to the tariffs was announced which allowed negotiations to continue and eased confusion for businesses. The market recovery continued in the weeks that followed despite little progress on trade agreements and a war in the Middle East that included American intervention. In the final weeks of the quarter, the focus was on proposed legislation aimed at extending tax cuts among other policy objectives like increasing defense and border security spending and cutting social safety net programs. The journey from trough to the end of the quarter was a resounding 25%.

The Bond Market

The bond market returned 1.21% for the second quarter, bringing the return for the first half of 2025 to 4.02%.1 While the Fed hasn’t continued cutting the Federal Funds Rate, leaving most short-term rates relatively unchanged, longer term rates have been far less steady. At times, longer term rates, which are determined by market supply and demand, actually increased. It’s difficult to know the exact reasons but some speculated an unwinding of holdings from large holders such as China or Japan.2 Others speculated it was due to the ballooning deficit which led Moody’s to downgrade U.S. credit from AAA to AA.3 In any case, it is something to watch as the recently passed tax bill will add an estimated $3.4 trillion to the deficit.4 Investors may expect higher yields as the U.S. continues to borrow, which would in turn lead to higher long-term rates for all other borrowers (e.g. mortgages, auto loans, business loans, etc.). It’s definitely something to keep an eye on.

What’s Ahead

While some tariffs have been implemented, the start date for many of the larger tariffs continues to get postponed to allow more time to negotiate trade agreements county-by-country. It’s unclear when or even if those higher tariffs could come into play. Many companies also increased their inventories before the tariffs took effect and are still offloading their excess reserves allowing them to avoid the tariffs for a while. Is the market pricing in enough downside risk that the tariffs get fully implemented and refuel inflation and/or decrease consumer spending power leading to a recession? Probably not, but it’s also difficult to bet against the market when we could have two cuts to interest rates this year (the Fed’s base case5) not to mention a pattern of delaying tariffs that could spook the markets. So, like the Fed, we approach the market with patience knowing it’s not as bad as some people make it out to be and not as good as others do. The wild ride has subsided for now and we’re seeing broad leadership grinding to higher highs which has provided solid footing for now.

Sources & Disclosures

1. Data from Kwanti.com based on the S&P 500 Total Return index

2. https://www.cnbc.com/2025/04/15/us-treasurys-selloff-what-happened-and-why.html

3. https://ratings.moodys.com/ratings-news/443154

5. Federal Reserve, Summary of Economic Projections, June 18, 2025